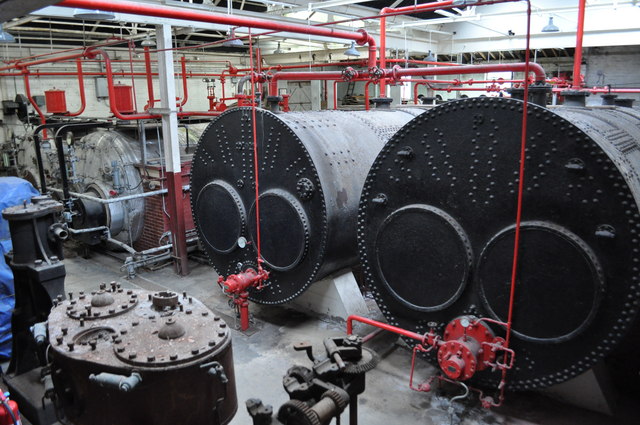

Overview

Boiler and machinery coverage—often marketed today as equipment breakdown insurance—covers sudden and accidental failures of mechanical, electrical, and pressure systems that standard property policies exclude. It combines property repair or replacement for covered equipment with inspection and loss-control services so businesses can recover quickly when critical systems fail. For industry-specific program options, see Hotel/Motel/Boiler and Machinery Insurance.

Boiler and machinery coverage—often marketed today as equipment breakdown insurance—covers sudden and accidental failures of mechanical, electrical, and pressure systems that standard property policies exclude. It combines property repair or replacement for covered equipment with inspection and loss-control services so businesses can recover quickly when critical systems fail. For industry-specific program options, see Hotel/Motel/Boiler and Machinery Insurance.

Key takeaways

- Equipment breakdown insurance fills gaps left by standard property policies, covering sudden mechanical and electrical failures.

- Policies often include inspection services that help prevent breakdowns and satisfy local inspection requirements.

- Coverage priorities include equipment repair, business income loss, spoilage, and extra expenses to keep operations running.

- Review equipment lists with an agent to match limits and endorsements to your operational risks.

How it works

Coverage is typically triggered by sudden, accidental mechanical or electrical breakdown, not by wear and tear or lack of maintenance. When a covered item fails, the policy pays to repair or replace the equipment and may also cover the resulting loss of income and extra expenses incurred to continue operations.

Inspections are a standard feature: trained technicians examine boilers, pressure vessels, refrigeration, generators, and other mission-critical machinery to identify risks and recommend maintenance or upgrades. These inspections both help reduce losses and support underwriting decisions.

For programs tailored to broader property portfolios that include equipment breakdown protection, you can review options such as International Property Insurance (including Boiler and Machinery).

What it may cover (and what it may not)

- Typical coverages:

- Repair or replacement of damaged boilers, compressors, chillers, HVAC, pumps, turbines, and electrical switchgear.

- Business income and extra expense to limit interruption losses.

- Spoilage of refrigerated stock and contamination events tied to equipment failure.

- Expedited repair or overtime costs to restore operations quickly.

- Common exclusions and limits:

- Damage caused by poor maintenance, gradual deterioration, corrosion, or wear and tear is usually excluded.

- Pre-existing defects known to the insured but not disclosed may be denied.

- Some policies limit coverage for electronic data loss or certain specialty equipment without specific endorsements.

Common mistakes to avoid

- Assuming standard property policies cover mechanical breakdown—this often leaves a gap for critical equipment losses.

- Failing to inventory and schedule all mission-critical equipment, which can lead to inadequate limits or missed exposures.

- Overlooking business income and extra expense coverages tied to equipment failure, which are often more consequential than the equipment damage itself.

- Skipping recommended inspections and maintenance that both reduce risk and support claim outcomes.

Questions to ask an agent

Ask what triggers the policy defines as a covered "breakdown" and whether wear-and-tear or maintenance failures are excluded. Request examples of covered losses similar to your operations and ask how business income and spoilage limits are calculated.

Confirm whether temporary power or rental equipment costs are included and whether there are sublimits for certain systems such as elevators or electronic controls. If you need industry-specific guidance, see Boiler & Machinery Insurance for Adult Care Facilities.

Next steps

Compile a list of boilers, chillers, refrigeration units, generators, HVAC systems, and other mission-critical machinery, including age, replacement cost, and maintenance history. Share this inventory with your insurance advisor and request a tailored equipment breakdown quote and recommended endorsements.

After reviewing options and limits, schedule the insurer’s inspection and align your maintenance program with their recommendations. To start the quote process, ask your agent for equipment breakdown coverage details and available endorsements.

Frequently Asked Questions

What is the difference between boiler and machinery insurance and standard property insurance?

Boiler and machinery (equipment breakdown) insurance covers sudden mechanical and electrical failures that standard property policies typically exclude, including repairs, business income, and related extra expenses.

Will the policy pay for spoiled inventory from a refrigerator failure?

Yes, many equipment breakdown policies include spoilage coverage for refrigerated stock when the loss is caused by a covered breakdown or power interruption.

Do I need regular inspections to keep coverage?

Inspections are commonly required and recommended because they help prevent losses and may be a condition of coverage or favorable underwriting terms.

How are business income losses calculated after a mechanical breakdown?

Business income coverage typically reimburses lost net income and necessary continuing expenses during the period of restoration, subject to policy limits and waiting periods.